Blog

Investments Retirement Taxation

Making the most of pension contributions before the end of the tax year for higher earners

Let’s look at how you can use your pension to keep more of your earnings in your pocket, especially if you have been pulled into a new tax threshold through a pay rise or new role.

Although salaries have been steadily increasing, tax thresholds have not. In the recent Budget, the Government confirmed the freeze on income tax thresholds has been further extended until 2031.

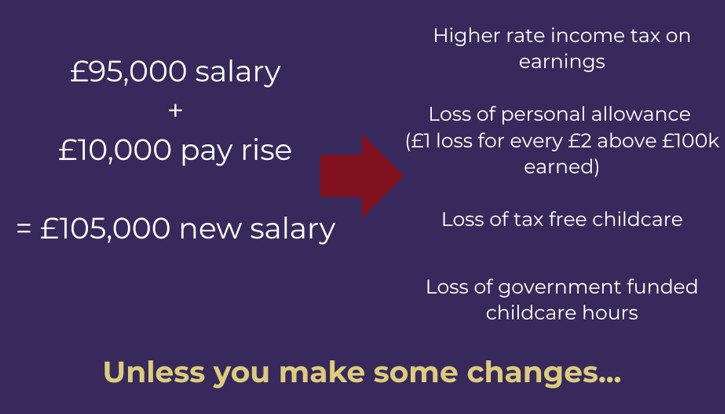

If your income exceeds £100,000, the rate of Income Tax you pay will be affected by the gradual removal of the personal allowance, tapered at a rate of £1 for every £2 earned above £100,000. This means if your income exceeds £125,140 you will have lost your entire Personal Allowance and is an effective 60% tax rate on income between £100,000 and £125,400.

Crossing a tax threshold not only affects the rate of tax you pay on your income but also the amount you pay on your savings. As a higher-rate taxpayer, your personal savings allowance of £1,000 halves to £500, whilst it vanishes completely if you become an additional-rate taxpayer.

That’s before you think about the impact to the family purse if you have children in childcare and you lose Government-funded hours and tax-free childcare entitlement.

What can you do?

In short, increase your personal pension contributions! The added incentive of receiving tax relief at your highest rate of tax is attractive, meaning your pot grows bigger, faster, and annual contribution limits for pensions are also quite generous.

When paying into a personal pension, the scheme will claim 20% tax relief on your behalf. You can then claim the extra 20% or 25% from HMRC through a Self-Assessment, depending on the rate of tax you pay. This reduces the overall cost of the contribution whilst growing your overall pot.

The annual allowance (the contributions you make, plus any your employer or third parties make for you) currently stands at £60,000 (or 100% of your annual earnings if lower) for most people. Unused annual allowance can usually be carried forward for up to three years, although the tax relief on personal contributions remains limited by earnings in that year.

Maxing out your pension contributions, alongside fully using your ISA allowance, means you’ll get the full benefit of your annual tax allowances, helping to reduce your annual tax bill and bringing you back under £100,000 adjusted net income with all the savings that brings, all while saving for the future.

Salary Sacrifice changes

From 6 April 2029, the National Insurance (NI) exemption for salary sacrifice pension contributions will be capped at £2,000 per tax year, following changes proposed in the Autumn 2025 Budget. Contributions exceeding this amount will become subject to Class 1 employee and employer NI, reducing the current tax efficiency for high savers.

For example, an employee earning £60,000 and contributing £3,000 via salary sacrifice (a £1,000 excess over the cap) would pay an additional £20 per year in NI.

The bigger impact will come for higher earners who often ‘sacrifice’ annual bonuses through salary sacrifice pension contributions. By putting earnings directly in pension pots before tax and NI are deducted, employees can reduce income tax paid, protect tax-free childcare, and drop down the tax thresholds, so it’s quite an attractive option.

This proposed change means that from 6 April 2026 there are three tax years to make the most of salary sacrifice pension contributions before the tax efficiency is reduced. So it’s worth speaking to your financial adviser soon to put a plan in place.

Protecting tax-free childcare

Losing tax-free childcare and Government-funded childcare hours has a huge impact on family finances. So, if you are over the £100,000 expected adjusted net income threshold (per parent and including bonuses) it is essential to look at options to shelter this support for working parents.

Most of us welcome a pay rise, but just a £10,000 pay rise could trigger a cascade of losses. On paper, you’re better off, but in reality, crossing the £100,000 threshold results in:

Making pension contributions is a great way to help protect your entitlement since making personal contributions into your pension reduces your adjusted net income.

If you are still above £100,000 in adjusted net income once you have maxed out your pension contributions, you could also consider making donations to a qualifying charity to bring you back under the threshold.

How can we help?

Accession specialises in providing high-quality, face-to-face wealth management advice for farmers, professionals, rural businesses and families across Bedfordshire, Cambridgeshire, Northamptonshire and the surrounding counties.

All three Accession financial advisers – Emma Wilcock, Joe Moricca and Richard Jones - are Chartered Financial Planners and Fellows of the Personal Finance Society, accolades held by a very small number of financial advisers in the UK and meaning we are fully equipped to help guide you through planning for the future. They are also all Top-Rated Financial Advisers with VouchedFor, the independent review platform for professional services.

If you or someone you know would benefit from speaking to one of our advisers about retirement planning, please do contact us on 01832 279170 or accession@sjpp.co.uk to discuss your requirements and get an appointment in the diary.

The value of an investment with St. James’s Place will link directly to the performance of the funds selected and may fall as well as rise. You may get back less than the amount invested.

The levels and bases of taxation, and reliefs from taxation, can change at any time and are generally dependent on individual circumstances.

SJP Approved 11/3/2026